Key Takeaways

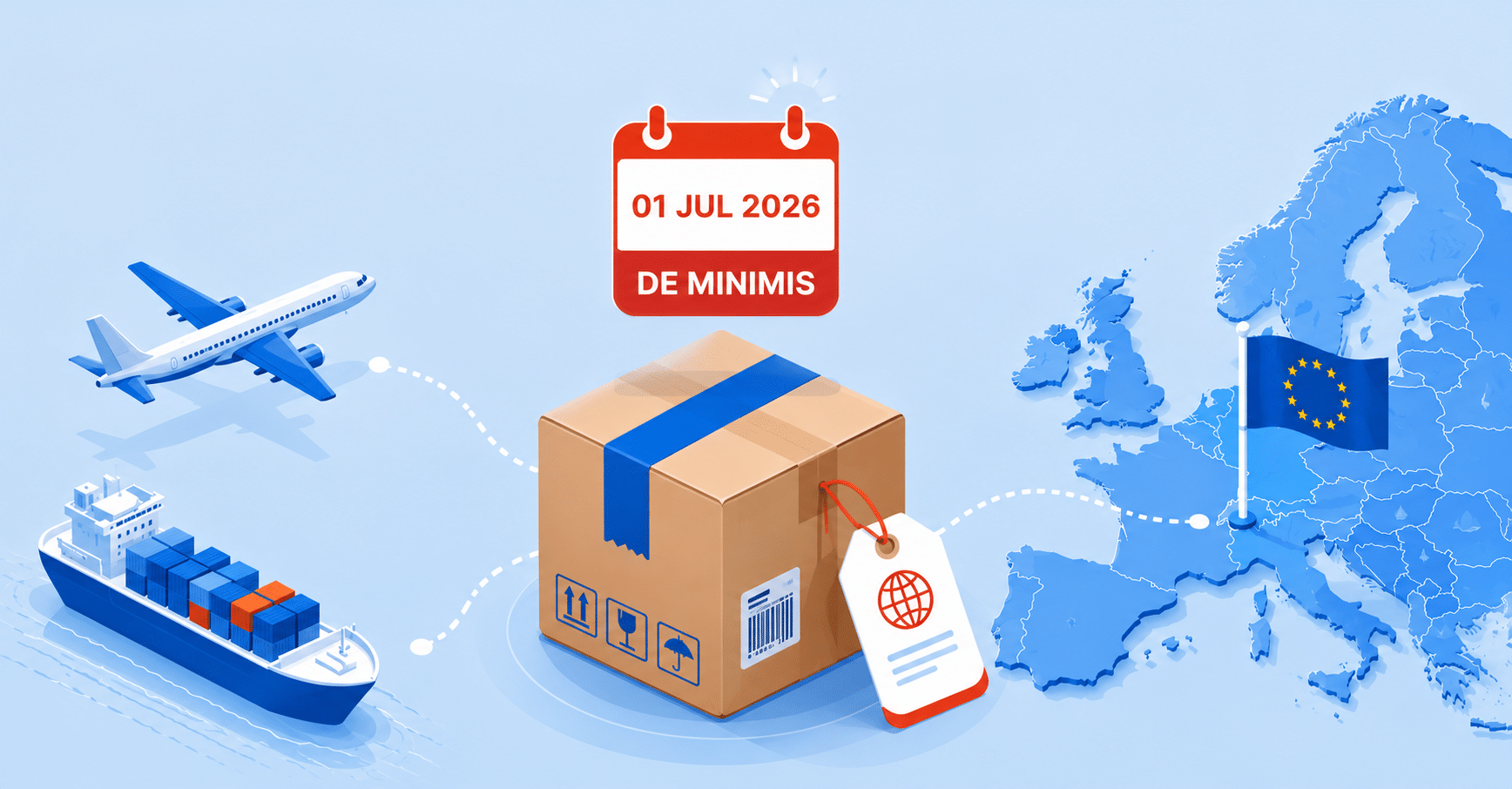

- €150 customs duty exemption ends on 1 July 2026

- €3 duty applies per tariff line

- IOSS and OSS remain unchanged

- Direct-shipping costs may increase

- Tariff classification becomes more important

- Centralised EU fulfilment may become more attractive

- Belgium and the Netherlands offer VAT deferment options

Why the New Duty May Challenge Existing Direct-Shipping Models

Although the €3 duty may appear relatively modest when viewed in isolation, its impact should be assessed in the context of the business models that currently dominate a significant portion of cross-border e-commerce imports into the European Union. Many non-EU sellers rely on large volumes of low-value consignments shipped directly from third countries to consumers across the EU, often operating on relatively narrow margins and highly optimised pricing structures.

In this context, the introduction of a fixed customs duty on low-value imports may result in a cumulative increase in landed costs, particularly where businesses process substantial numbers of individual orders. While the extent of the impact will vary depending on factors such as product value, shipment volumes and product mix, the additional cost may require businesses to reassess pricing strategies and overall cost allocation.

Beyond the financial implications, the measure may also increase operational complexity. Since the €3 duty is applied per tariff line, the customs treatment of a consignment will depend on the classification of the goods it contains. As a result, accurate tariff classification and reliable product-level customs data become increasingly important. This applies in particular to businesses managing high volumes of direct-to-consumer shipments from third countries into the EU. Businesses may therefore need to evaluate not only the direct cost of the new duty, but also the broader operational implications associated with maintaining high-volume direct-shipping models.

For a more detailed overview of the abolition of the customs duty exemption for low-value consignments imported into the European Union from third countries, and its broader customs implications, please refer to our dedicated article: EU Ends €150 Customs Exemption: €3 Duty on Small Parcels

Looking Beyond VAT Compliance

It is important to note that the introduction of the €3 customs duty does not alter the functioning of the EU VAT simplification regimes. The Import One-Stop Shop (IOSS) continues to provide a mechanism for the collection and reporting of VAT on eligible low-value imports into the European Union, while the One-Stop Shop (OSS) remains applicable to qualifying intra-EU B2C supplies.

The new customs duty highlights the separation between VAT and customs obligations. While IOSS addresses VAT collection at import, the €3 duty applies independently under the customs framework. As a result, this measure introduces an additional cost element that sits outside the scope of existing VAT simplification mechanisms, while still operating within the same underlying transaction flow, namely low-value B2C consignments imported into the European Union from third countries.

In this context, businesses may wish to assess VAT, customs and logistics considerations within a single operational approach rather than as separate compliance streams. While the relevance of IOSS as a VAT mechanism remains unchanged, the broader cost structure of importing goods into the EU may prompt a reassessment of end-to-end fulfilment models.

For a detailed overview of the Import One-Stop Shop (IOSS), its scope and practical operation, please refer to our dedicated article: What Is IOSS? Guide for Non-EU Sellers

An Alternative Model: Centralised EU Fulfilment with OSS Reporting

Against this background, some businesses may consider whether a more centralised import structure could, in certain cases, offer a viable alternative to fragmented direct-to-consumer shipping from third countries into the European Union. In particular, where business models rely on high volumes of low-value parcels, consolidating import flows at an EU entry point may reduce exposure to per-consignment customs costs and support more structured customs handling.

Under such an approach, goods are no longer shipped individually to end customers from outside the EU but are instead imported in bulk into a single EU-based entry point. This typically involves the establishment of a VAT registration in an EU Member State and, where required, the appointment of a fiscal representative to manage local compliance obligations. Once imported, goods are released into free circulation within the EU and stored within a distribution hub for subsequent intra-EU B2C sales.

From a VAT perspective, intra-EU distance sales to consumers in different Member States may then be reported through the One-Stop Shop (OSS), allowing for a centralised declaration of VAT across multiple jurisdictions. In this context, the compliance focus shifts from individual import transactions to a more consolidated reporting model at EU level.

Operationally, this structure may offer greater predictability in terms of customs processing, as import formalities are concentrated at a single point rather than distributed across multiple small consignments. It may also allow for improved control over product data, classification consistency and supply chain visibility. In certain cases, it may additionally facilitate more stable cash-flow management depending on the import VAT accounting treatment available in the chosen Member State.

Overall, this model does not replace existing IOSS-based solutions but may represent an alternative operational configuration for businesses whose current direct-shipping model is increasingly affected by cumulative customs costs and administrative complexity.

Belgium and the Netherlands as Potential Gateways

Under a centralised import model, non-EU businesses typically consolidate importation into a single EU entry point, where goods are cleared in bulk, placed into free circulation and subsequently stored in an EU-based warehouse for distribution within the Union. This structure requires a VAT registration in the Member State of importation and, where applicable, the appointment of a fiscal representative to ensure compliance with local VAT and customs obligations. Intra-EU B2C sales are then carried out from the EU warehouse and reported through a local VAT registration, with OSS reporting applied for cross-border supplies within the Union.

The selection of the EU import entry point plays a relevant role in the design of a centralised import structure, as it influences the practical handling of import VAT, customs clearance procedures and the efficiency of downstream distribution flows within the Union. In particular, the availability of import VAT deferment mechanisms and simplified accounting procedures may have a material impact on liquidity management and operational efficiency in high-volume import scenarios.

Within this context, Belgium and the Netherlands are frequently assessed as viable entry jurisdictions for such structures. Belgium offers mechanisms such as the ET 14.000 licence, which allows for deferred accounting of import VAT under specific conditions, while the Netherlands applies a comparable approach through the Article 23 licence, enabling import VAT deferment at the point of importation. These mechanisms may support more efficient cash-flow management and facilitate the alignment between customs processes and EU-wide distribution models.

For a more detailed analysis of the ET 14.000 licence and its operational implications, please refer to our dedicated article: Belgium ET 14.000: Improve Import VAT Cashflow

How Gerlach Customs Can Support

Gerlach works with businesses at each stage of this process, from reviewing existing import and distribution models to supporting the design of centralised EU import structures. This includes VAT registrations and fiscal representation in Belgium, the Netherlands and other EU Member States, OSS registration and compliance, and advisory support on customs and supply chain design for cross-border e-commerce. Get in touch to discuss your current fulfilment setup.